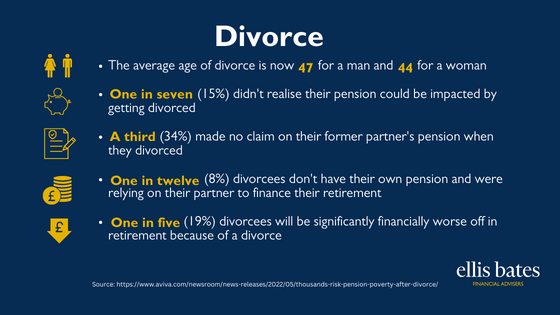

Divorce and my Pension

https://www.ellisbates.com/wp-content/uploads/2023/01/Pensions-and-Divorce-560-×-315px.png 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=g

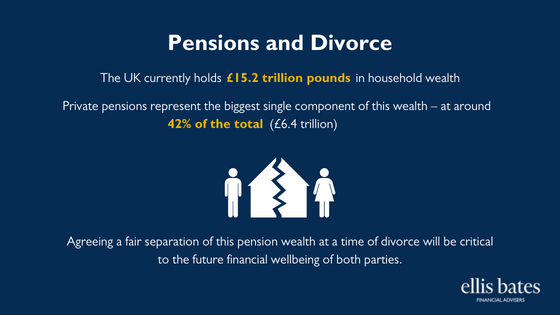

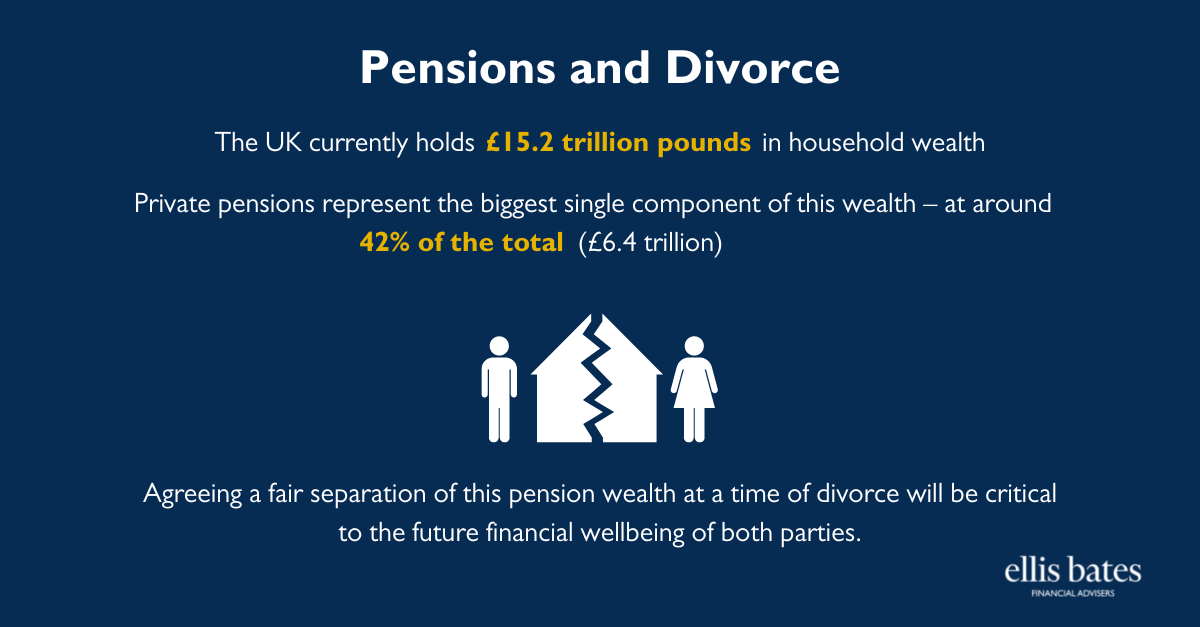

- The UK currently holds £15.2 trillion pounds in household wealth

- Private pensions represent the biggest single component of this wealth – at around 42% of the total (£6.4 trillion)

- Agreeing a fair separation of this pension wealth at a time of divorce will be critical to the future financial wellbeing of both parties

If you’re going through a divorce and would like to discuss your options regarding your pensions then please contact us.