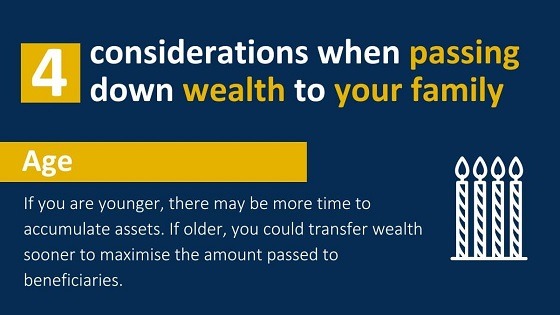

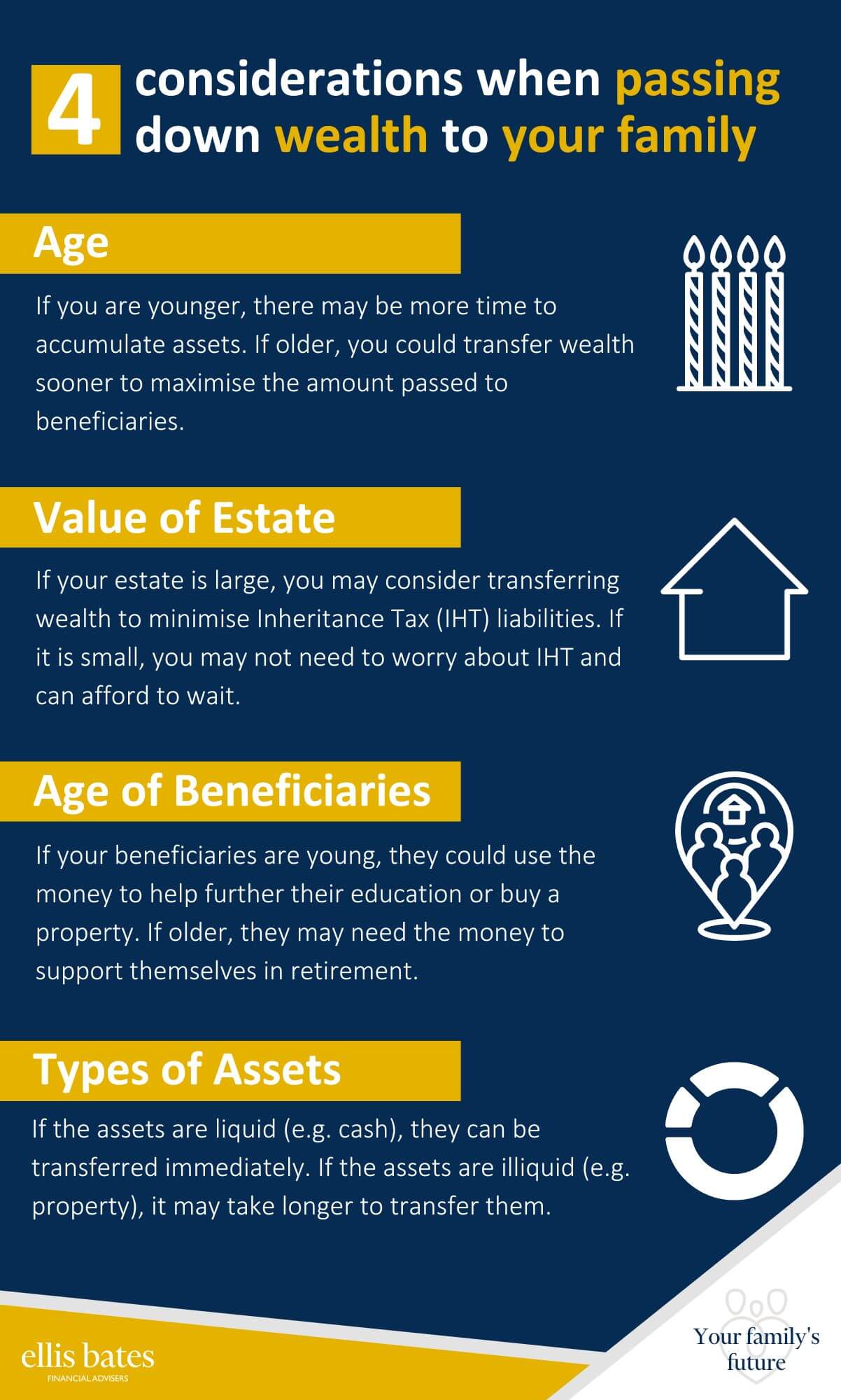

The importance of drafting a Will

https://www.ellisbates.com/wp-content/uploads/2023/07/Why-do-I-need-an-LPA.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=gProtect your family from uncertainty and potential conflicts

Many people still lack a properly organised estate plan despite the numerous benefits of writing a Will—such as getting our finances in order, planning our legacy, and ensuring that our loved ones are well looked after.

Many people still lack a properly organised estate plan despite the numerous benefits of writing a Will—such as getting our finances in order, planning our legacy, and ensuring that our loved ones are well looked after.

By taking the proactive step to draft a Will, you can protect your family from uncertainty and potential conflicts, ensuring that your legacy is preserved according to your exact intentions. If you haven’t done so already, now is the time to prioritise this important task and secure the future for those you care about most.

A way to get assets in order

Making a Will often prompts a financial review. It typically identifies gaps in people/s financial planning – often inadequate life assurance or disability income benefit cover. If they’re in an occupational pension scheme, they may need to update their nomination of beneficiaries form. Without a Will, Intestacy laws determine who inherits your estate and in what order.

If you don’t have a valid Will, then effective state legislation steps in and provides a series of rules with you may not wish to apply to your assets and your family. It’s also relatively inexpensive compared to the problems you can create for your family without making a Will.

Specifying sentimental gifts in your Will

We dedicate much of our lives to working hard to provide for ourselves and our loved ones. As we accumulate assets and cherished possessions over time, it becomes crucial to ensure that they are distributed according to our wishes when we are no longer around. Importantly, the gifts mentioned in a Will do not need to be limited to property or cash. This can also include sentimental items with significant emotional value but less material worth, These could be family heirlooms, personal mementoes, or any treasured possessions that we wish to pass down to future generations. By specifying these sentimental gifts in our Will, you ensure that these meaningful items are handed down to those who will appreciate them most.

Leave money to a good cause

While family and friends are likely to be the first considerations when writing a Will, many people also take the opportunity to give a helping hand to causes close to their hearts. For many charities, gifts in Wills account for a significant amount of their income. Without these legacies, much of their work would not be possible. Leaving money to charity could also cut your Inheritance Tax bill.

Some charities will even help you write a Will if you leave them a donation. By leaving 10% of the value of your estate to a charity, you could reduce Inheritance Tax payable on some of your assets from 40% to 36%.

You choose the legal guardians

A Will allows you to appoint one or more legal guardians for children aged under 18. Your chosen guardians will take over the role of bringing up the children on your behalf. This ensures you remain in control and entrust this significant responsibility to people you deeply trust. In addition, having a Will grants you the peace of mind that comes with knowing your children’s future is secured. By choosing guardians, you ensure they are cared for by individuals who share your values and vision for their upbringing.

You choose the executors

Choosing your own executor, the individual responsible for implementing the terms of your Will, can ensure that your estate is distributed by someone you trust. You can appoint people you know and rely on to be your executors and manage your estate. Alternatively, you can appoint professionals to serve as your executors. An executor plays a crucial role in managing your affairs posthumously, ensuring that your wishes are carried out accurately and efficiently. This includes settling debts, distributing assets, and handling other legal matters related to your estate.

“TAKING OUT A LIFE INSURANCE POLICY CAN FURTHER ENSURE THAT YOUR FAMILY IS FINANCIALLY SECURE. LIFE INSURANCE CAN SERVE AS A SAFETY NET, PROVIDING FINANCIAL SUPPORT TO YOUR LOVED ONES IN THE EVENT OF YOUR PASSING.”

You ensure partners are looked after

There’s a common misconception that the rules provide for a ‘common-law’ husband or wife. If you’re unmarried or in a registered civil partnership and don’t have a Will, your partner won’t inherit anything under the laws of intestacy. A Will ensures that couples who live together but aren’t married or in a registered civil partnership can leave their assets to each other. Taking out a life insurance policy can further ensure that your family is financially secure. Life insurance can serve as a safety net, providing financial support to your loved ones in the event of your passing.

A Will should be updated

A Will should be reviewed at least every three years and whenever there’s a significant live event, such as the birth of a child or when children become adults. Keeping your Will up to date ensures that it reflects your current wishes and circumstances. Amending a Will is straightforward – you can rewrite parts of it with something called a codicil. This allows you to make minor adjustments without drafting a completely new document.

Peace of mind

Making a Will can relieve a considerable burden on your mind. Completing a properly-arranged Will provides peace of mind, knowing that your assets will be distributed according to your wishes. Writing a Will places you in the driver’s seat for many important decisions, impacting not just your life but also those of your family and friends.

Once written, many people feel great relief, especially when they can cross it off their ‘to-do’ list. However, remember to update it as needed to ensure it remains relevant.

Looking to draft or update an existing Will?

Please contact us for further information on drafting a comprehensive Will and safeguarding your legacy for future generations. Whether you’re just beginning the process or looking to update an existing Will, we’ll help you navigate every step confidently and easily.

Protecting your legacy and boosting your children’s financial security

Protecting your legacy and boosting your children’s financial security