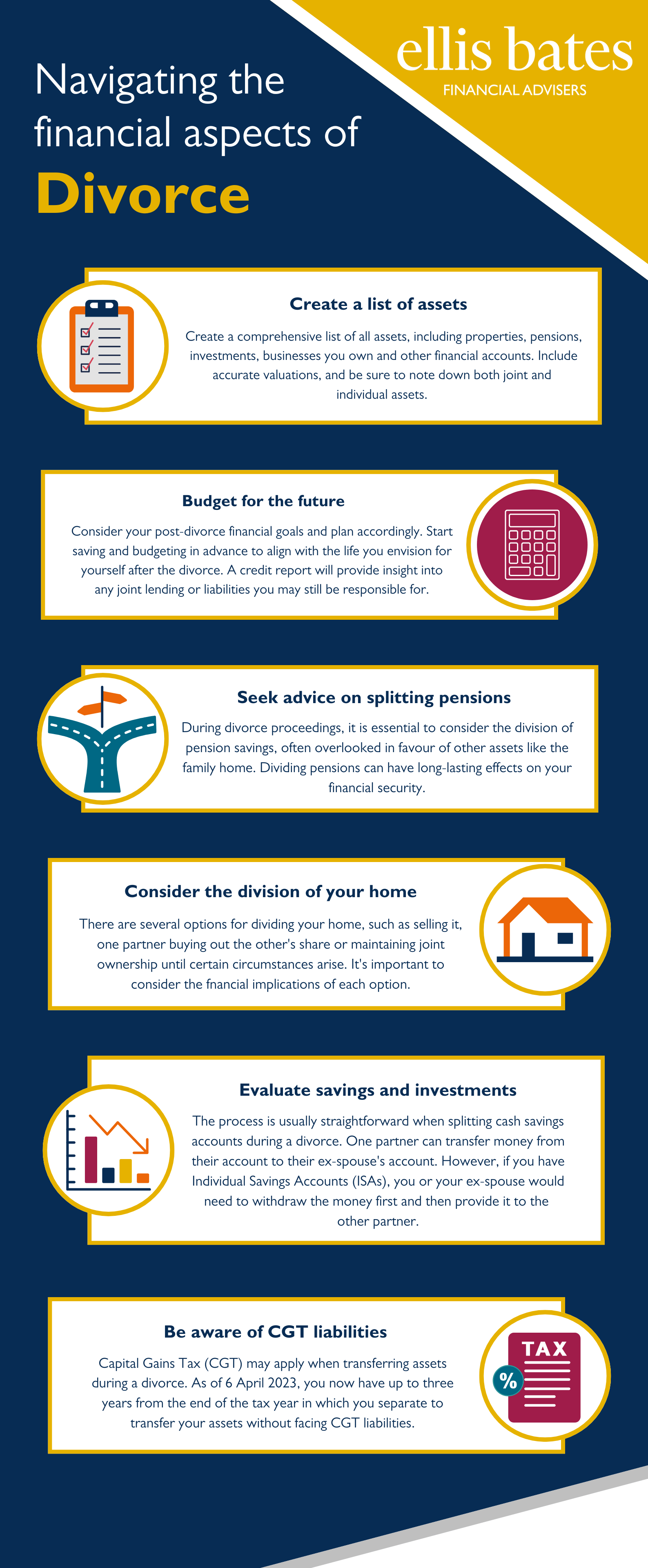

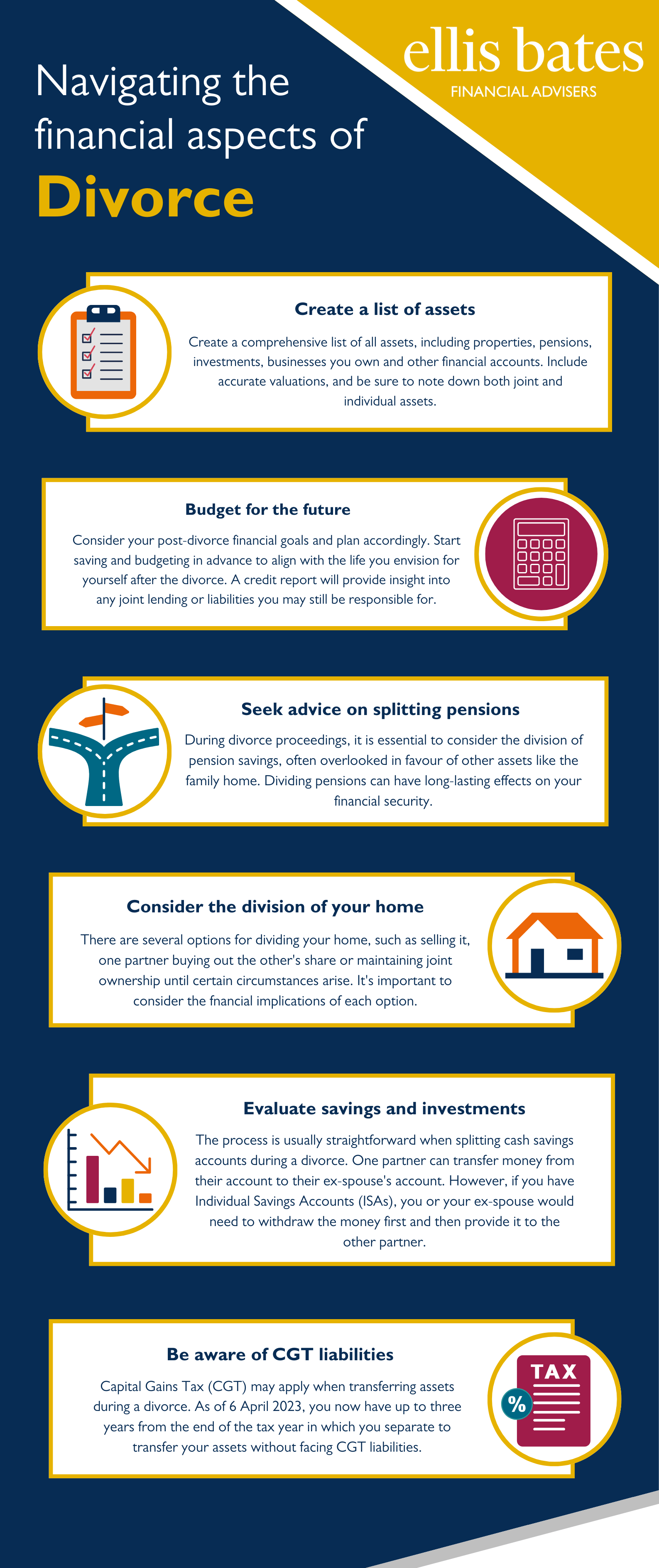

Financial advice during Divorce

https://www.ellisbates.com/wp-content/uploads/2024/10/Ebookbrochure-socials-9-1024x535.png 1024 535 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=gDivorce can be bewildering, especially when managing your finances. However, understanding your options can make the process more manageable. Financial concerns may not be your first thought during a marital breakdown. Still, given the significant impact divorce can have on your financial future, it’s crucial to take proactive steps to safeguard your financial security.

Download our guide to Financial advice during Divorce to find out how you can secure your future.