Saving for retirement

https://www.ellisbates.com/wp-content/uploads/2023/07/6-tips-for-saving-for-retirement-infographic-holder.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

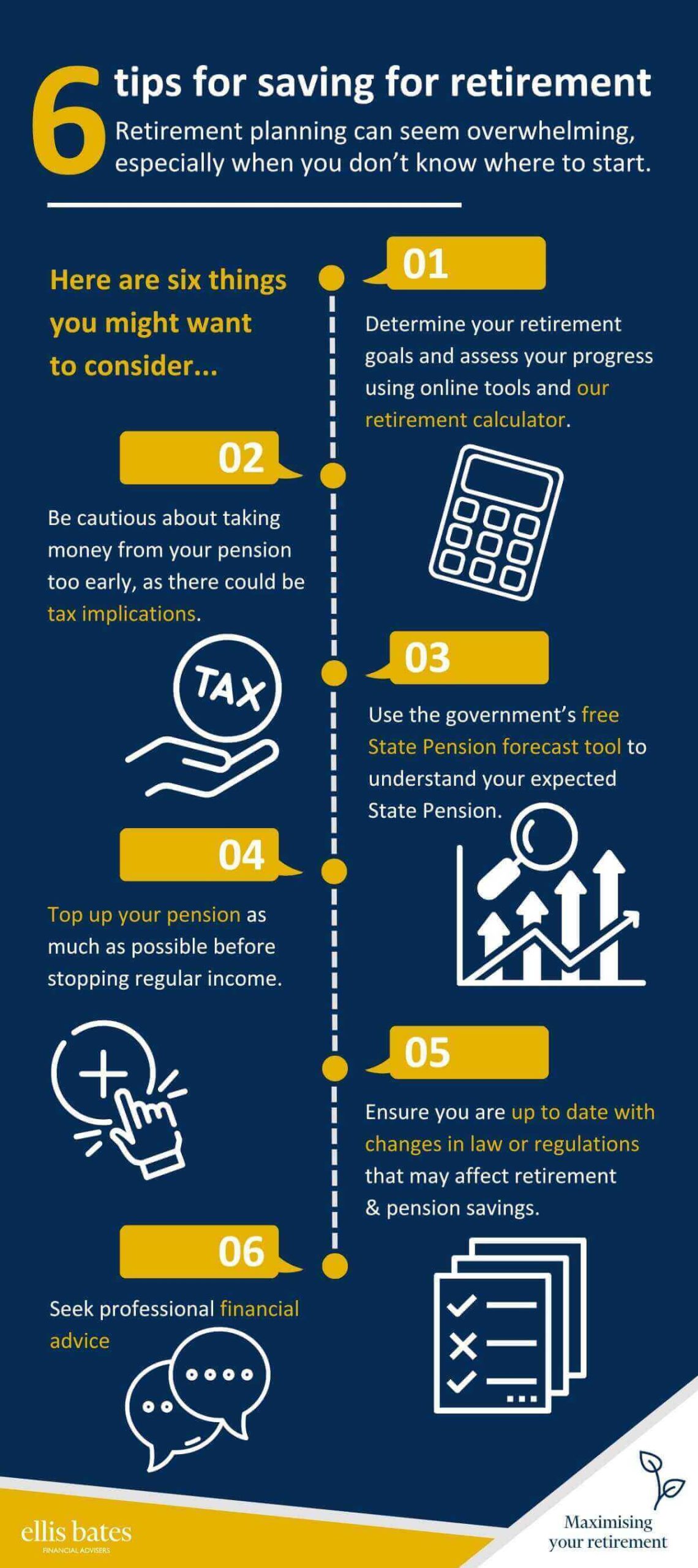

Retirement planning can seem complex and overwhelming. We have some top tips that you might want to consider if you are planning for your retirement:

- Use online tools and our retirement calculator to assess your retirement planning progress

- Consider any tax implications if you are thinking about taking money from your pension too early

- Visit the governments free State Pension forecast tool to understand your expected State Pension – https://www.gov.uk/check-state-pension

- Top up your pension as much as you can before you stop regular income

- Check you are up to date with any changes in the law or regulations that may affect your retirement and pension savings

- Seek professional financial advice

Read our article on “how much do I need to retire?” for more information on retirement planning.