Financial Gifting

https://www.ellisbates.com/wp-content/uploads/2022/12/Gifting-560-×-315px.png 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

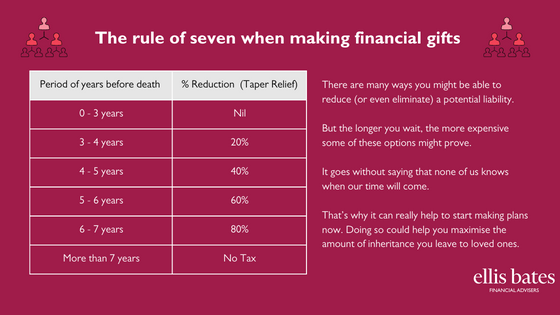

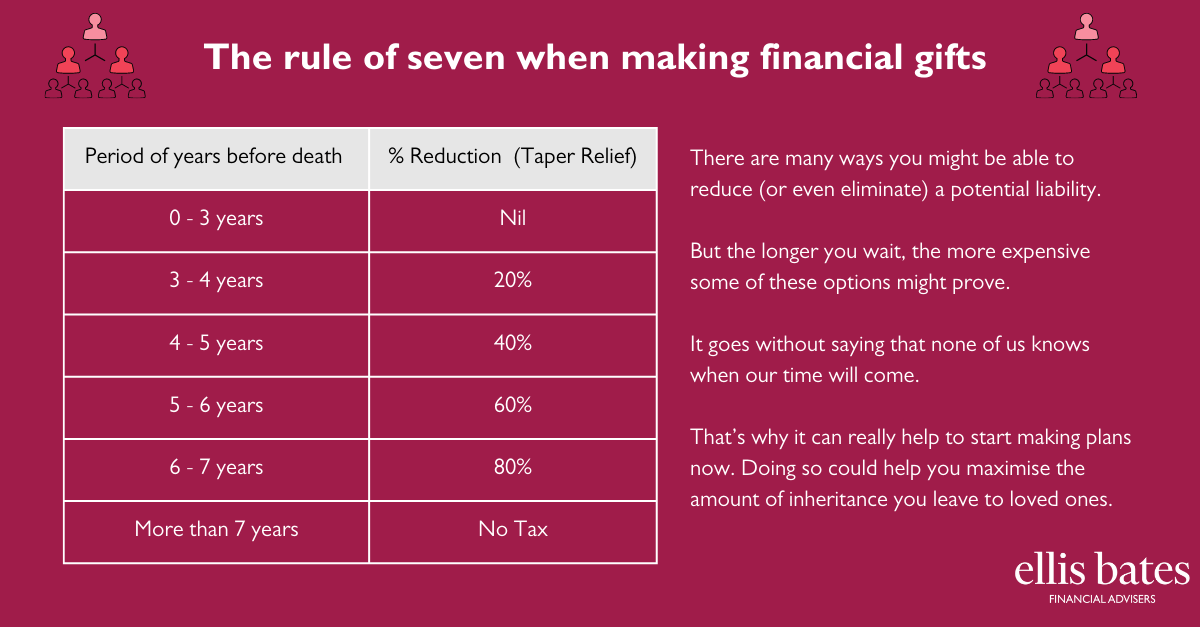

The rule of seven when making financial gifts

There are many ways you might be able to reduce (or even eliminate) a potential liability.

But the longer you wait, the more expensive some of these options might prove.

It goes without saying that none of us know when our time will come.

That’s why it can really help to start making plans now. Doing so could help you maximise the amount of inheritance you leave to loved ones.

Why parents should look to Christmas investment gifts instead of toys.

Why parents should look to Christmas investment gifts instead of toys.