Enhancing pension contributions for a brighter future

https://www.ellisbates.com/wp-content/uploads/2024/05/GettyImages-1282867856-1024x523.jpg 1024 523 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

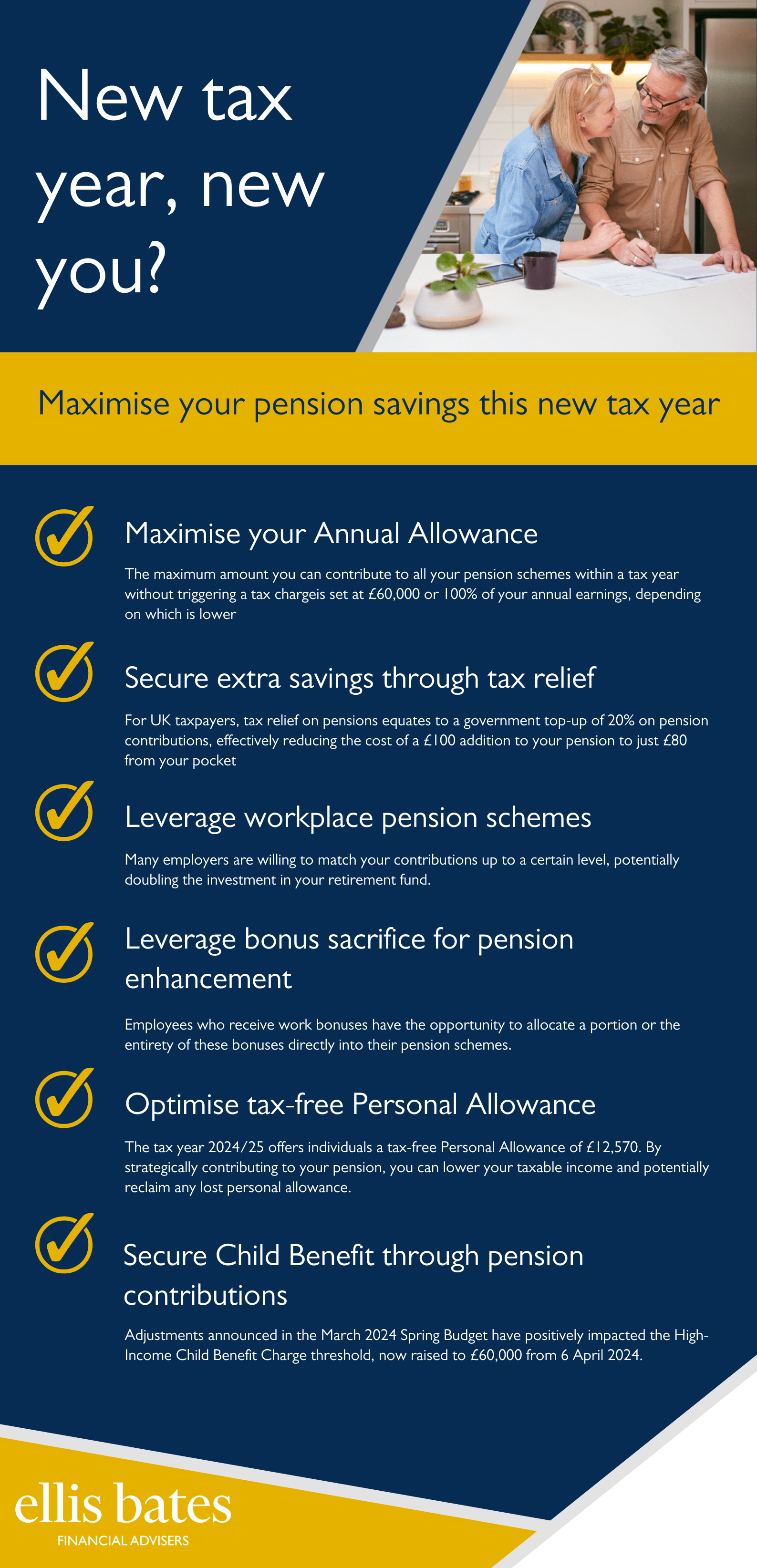

New tax year, new you? Maximise your pension savings this new tax year

As we embark on the new tax year, it presents an opportune moment to review your pension savings strategy, setting a solid foundation for future financial stability. Early attention to your private pension at the onset of the fiscal year is not just about cultivating beneficial saving habits; it’s also about ensuring you fully exploit the benefits and allowances available to you.

Delaying until the end of the tax year might seem convenient, yet acting early and promptly in this new tax year allows your investments more time to grow. Leveraging the power of compound growth can significantly bolster your pension pot and, by extension, your retirement prospects.

Maximising your Annual Allowance

The annual pension allowance represents the maximum sum that your employer, you as the individual and any external parties can contribute to all your pension schemes within a tax year without triggering a tax charge. As established last year, this cap is set at £60,000 or 100% of your annual earnings, depending on which is lower.

For those without earnings, the maximum tax relievable contribution would be £3,600 gross, and for individuals who have commenced withdrawals from their pension funds, they might face the Money Purchase Annual Allowance, lowering their allowance to £10,000. If your financial situation permits, maximising your pension contributions early in the tax year enables you to fully utilise the annual allowance and potentially reduce your tax liability if your earnings are equal to the annual allowance or more.

Securing extra savings through tax relief

Tax relief stands as a compelling incentive, rendering pension plans amongst the most tax-efficient vehicles for retirement savings. For the majority of UK taxpayers, this equates to a government top-up of 20% on pension contributions, effectively reducing the cost of a £100 addition to your pension to just £80 from your pocket.

Higher and additional rate taxpayers may be entitled to further relief, though claims beyond the basic rate require a self-assessment tax return. It’s worth noting that some workplace pensions may apply tax relief differently, such as through salary sacrifice schemes, so it’s advisable to verify the specifics with your employer.

Leveraging workplace pension schemes

Workplace pension schemes significantly enhance your ability to save for retirement, with compulsory contributions from both you and your employer. A minimum total contribution of 8% of your qualifying earnings is required, including at least a 3% contribution from your employer.

Many employers are willing to match your contributions up to a certain level, potentially doubling the investment in your retirement fund. Investigating whether increasing your contributions could lead to higher employer contributions is an astute strategy for maximising your pension growth.

Leveraging bonus sacrifice for pension enhancement

In the realm of financial planning, particularly regarding retirement savings, the concept of bonus sacrifice stands out as a strategic manoeuvre. Employees who receive work bonuses have the opportunity to allocate a portion or the entirety of these bonuses directly into their pension schemes.

Some employers may be willing to match your contributions up to a certain level, potentially doubling the investment in your retirement fund. Investigating whether increasing your contributions could lead to higher employer contributions is an astute strategy for maximising your pension growth.

Optimising tax-free Personal Allowance

The tax year 2024/25 offers individuals a tax-free Personal Allowance of £12,570, a crucial figure in personal finance management. However, this allowance decreases by £1 for every £2 of income above £100,000, ultimately disappearing once income surpasses £125,140.

By strategically contributing to your pension, you can lower your taxable income and potentially reclaim any lost personal allowance. This results in receiving tax relief at an effective marginal rate of 60%, a significant advantage for your pension contributions.

Securing Child Benefit through pension contributions

Adjustments announced in the March 2024 Spring Budget have positively impacted the High-Income Child Benefit Charge threshold, now raised to £60,000 from 6 April 2024. With the complete cancellation threshold also increased to £80,000, fewer families will find their Child Benefit reduced or nullified.

Enhancing pension contributions can effectively diminish taxable income for those with earnings within these brackets, thereby retaining Child Benefit entitlements. Even for earners above £60,000, applying for Child Benefit to accrue National Insurance credits remains beneficial, which is vital for the State Pension.

Unlike pension drawdown arrangements, annuities do not typically pass down any remaining funds to beneficiaries after the holder’s death. However, it is possible to balance security and flexibility by partially combining annuities with pension drawdown.

Unlike pension drawdown arrangements, annuities do not typically pass down any remaining funds to beneficiaries after the holder’s death. However, it is possible to balance security and flexibility by partially combining annuities with pension drawdown.

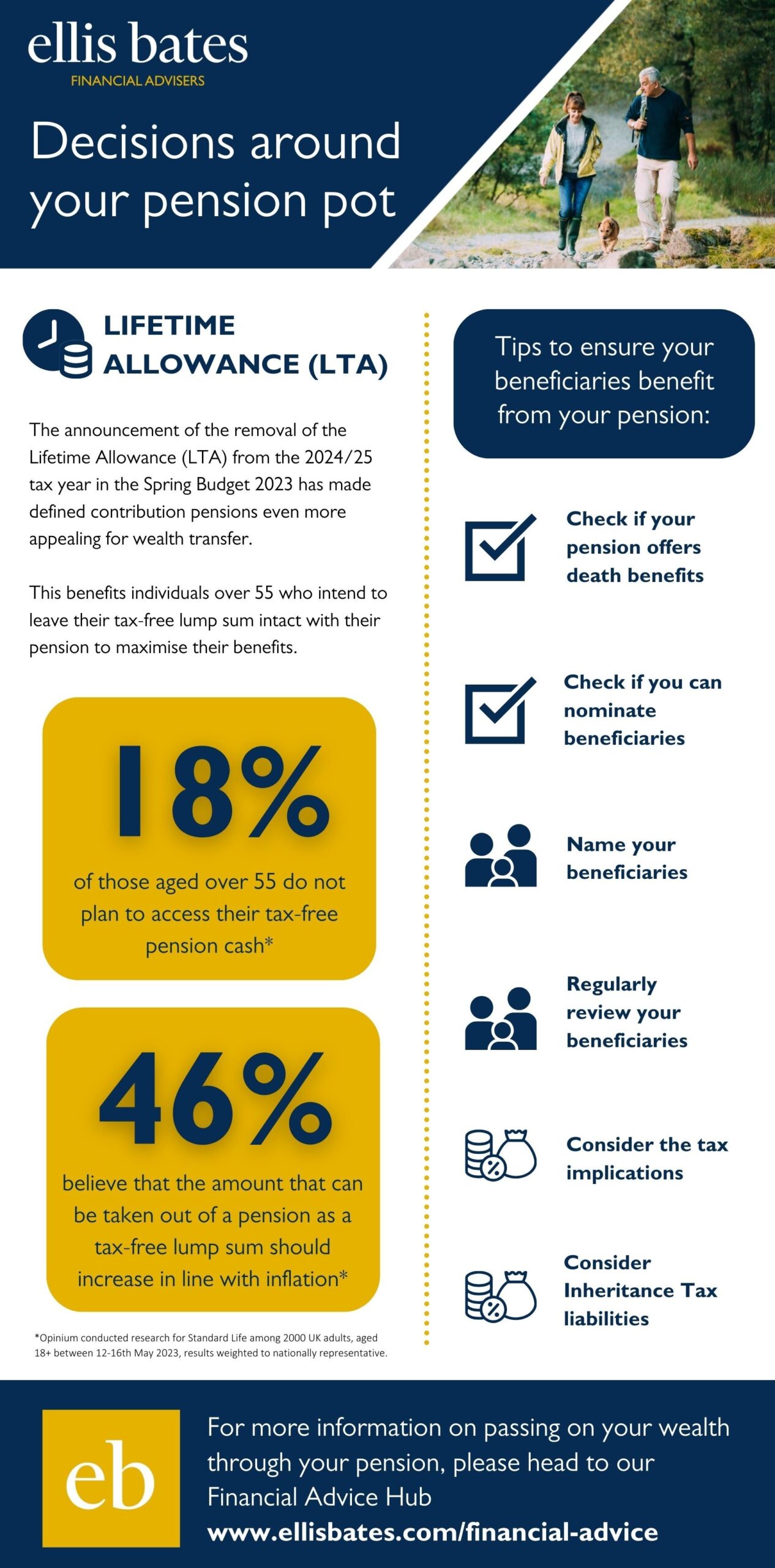

The announcement of the removal of the Lifetime Allowance (LTA) from the 2024/25 tax year in the Spring Budget 2023 has made defined contribution pensions even more appealing for wealth transfer. This benefits individuals over 55 who intend to leave their tax-free lump sum intact with their pension to maximise their benefits.

The announcement of the removal of the Lifetime Allowance (LTA) from the 2024/25 tax year in the Spring Budget 2023 has made defined contribution pensions even more appealing for wealth transfer. This benefits individuals over 55 who intend to leave their tax-free lump sum intact with their pension to maximise their benefits.