Inheritance Tax Receipts Reach £6.1 bn

https://www.ellisbates.com/wp-content/uploads/2023/01/IHT-Receipts.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/0e2a278e0eef1defdd7ee9d0ae7bb398?s=96&d=mm&r=g

Inheritance tax receipts reach £6.1 bn. What if I could make my wealth more tax-efficient?

We all want to leave a legacy and make sure the ones we care about most are well taken care of when we’re gone. That’s why Inheritance Tax planning is so important, to have confidence that your children, grandchildren and those you hold dearest will be taken care of long into the future.

Inheritance Tax is a tax on the estate of someone who has passed away. The standard Inheritance Tax rate is 40% in the current 2022/23 tax year. Your estate consists of everything you own. This includes savings, investments, property, life insurance payouts (not written in an appropriate trust) and personal possessions. Your debts and liabilities are then subtracted from the total value of your assets.

Passing on your main residence to direct relatives

Every person in the UK currently has an Inheritance Tax allowance of £325,000 (frozen until April 2026). This is known as the nil-rate band (NRB). In 2017, an extra allowance was introduced to make it easier to pass on your main residence to direct relatives (i.e. a child or grandchild) without incurring Inheritance Tax. This allowance is currently £175,000, known as the residence nil-rate band (RNRB), and is on top of the standard nil-rate band of £325,000.

A tapered withdrawal applies to the RNRB when the overall value of an estate exceeds £2 million. The withdrawal rate is £1 for every £2 over the £2 million threshold.

Allowed to use both tax-free allowances

If you are married or in a registered civil partnership, you are allowed to pass on your assets to your partner Inheritance Tax-free in most cases. The surviving partner is then allowed to use both tax-free allowances. Provided the first person to pass away leaves all of their assets to their surviving spouse, the surviving spouse will have an Inheritance Tax allowance of £650,000 (£1 million if they are eligible for the RNRB).

According to recent figures released by HM Revenue & Customs (HMRC), more estates in the UK are now paying Inheritance Tax than ever before[1].

Paying Inheritance Tax unexpectedly

Inheritance Tax receipts totalled £6.1 billion in the 2021/2022 tax year, up £729 million on the year prior. This 14% increase marks the largest single-year rise in Inheritance Tax receipts since the 2015/2016 tax year. The increase is the result of the ongoing freeze on the nil-rate Inheritance Tax band and residence nil-rate Inheritance Tax band.

Many more families are finding the total value of their estate – driven by a rapid growth in house prices, savings and other assets – is likely to be above £1million at the point of death, meaning many more estates could end up having to pay Inheritance Tax unexpectedly

Start conversation with your loved ones

In the 2019/20 tax year, there were 23,000 such deaths, up 4% on the year prior[1]. Given this data only covers to the start of the pandemic, this number is likely to have risen considerably over the past couple of years as asset prices grew.

With many more estates likely to be subject to an Inheritance Tax bill, it remains important that you have a conversation with your loved ones sooner rather than later so that you all fully understand your estate, the value of it and the potential to pay an Inheritance Tax bill.

Save your family thousands of pounds

When discussing your Will and any potential Inheritance Tax liability, there are things that can be put into place to mitigate or reduce a future payment.

That’s why planning for Inheritance Tax is a fundamental part of financial planning. It could potentially save your family thousands of pounds in Inheritance Tax payments when you die and ensure that your wealth is preserved for future generations.

What will your legacy look like?

We understand every situation is unique. We’ll help you to identify any specific issues and recommend the changes needed to help you meet your long-term wealth protection goals in the most tax-efficient manner. To find out more, please speak to us.

Source data: [1] https://www.gov.uk/government/statistics/inheritance-tax-statistics-commentary/inheritancetax-statistics-commentary

The Financial Conduct Authority does not regulate taxation and trust advice and will writing. Trusts are a highly complex area of financial planning. Information provided and any opinions expressed are for general guidance only and not personal to your circumstances, nor are intended to provide specific advice. Tax laws are subject to change and taxation will vary depending on individual circumstances.

Preserving your wealth and transferring it effectively.

Preserving your wealth and transferring it effectively.

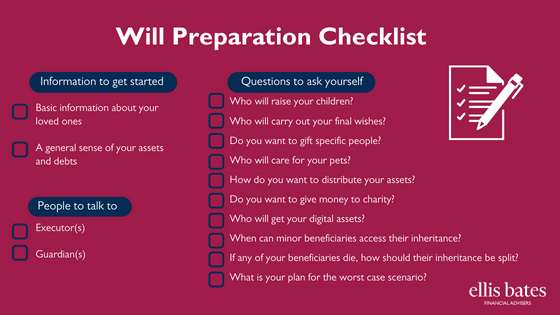

Over six million adults refuse to discuss their will with loved ones. Making a Will is very important if you care what happens to your money and your belongings after you die, and most of us do. But have you tried to talk with your children about your Will? If that conversation isn’t happening, you’re not alone.

Over six million adults refuse to discuss their will with loved ones. Making a Will is very important if you care what happens to your money and your belongings after you die, and most of us do. But have you tried to talk with your children about your Will? If that conversation isn’t happening, you’re not alone.