Millions of married couples have no idea about their spouse’s pensions & retirement plans

https://www.ellisbates.com/wp-content/uploads/2022/08/Retirement-taboo-holder.png 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

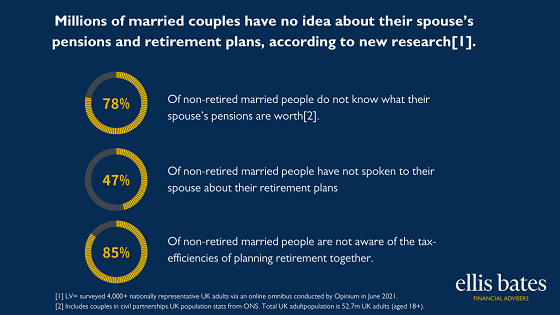

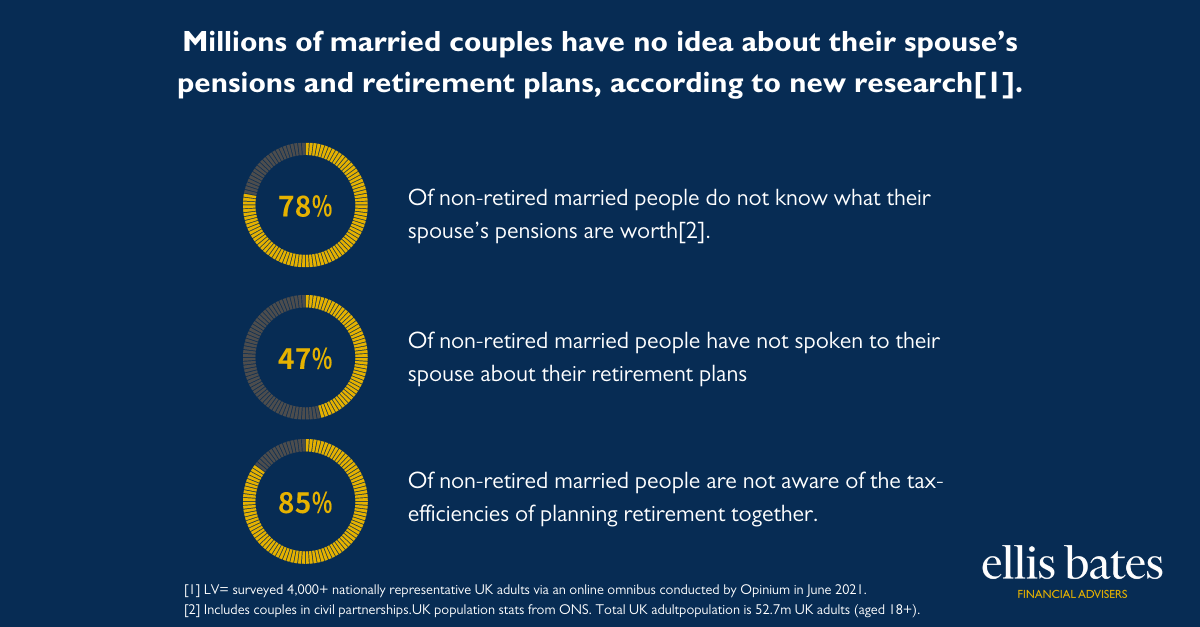

Millions of married couples have no idea about their spouse’s pensions and retirement plans, according to new research

78% of non-retired married people do not know what their spouse’s pensions are worth.

47% of non-retired married people have not spoken to their spouse about their retirement plans

85% of non-retired married people are not aware of the tax-efficiencies of planning retirement together

Why parents should look to Christmas investment gifts instead of toys.

Why parents should look to Christmas investment gifts instead of toys.

Steps towards a better financial future – grow, protect and transfer your wealth

Steps towards a better financial future – grow, protect and transfer your wealth

Financial Planning for your child’s future lifestyle. Early preparation in life is key to becoming financially independent.

Financial Planning for your child’s future lifestyle. Early preparation in life is key to becoming financially independent.