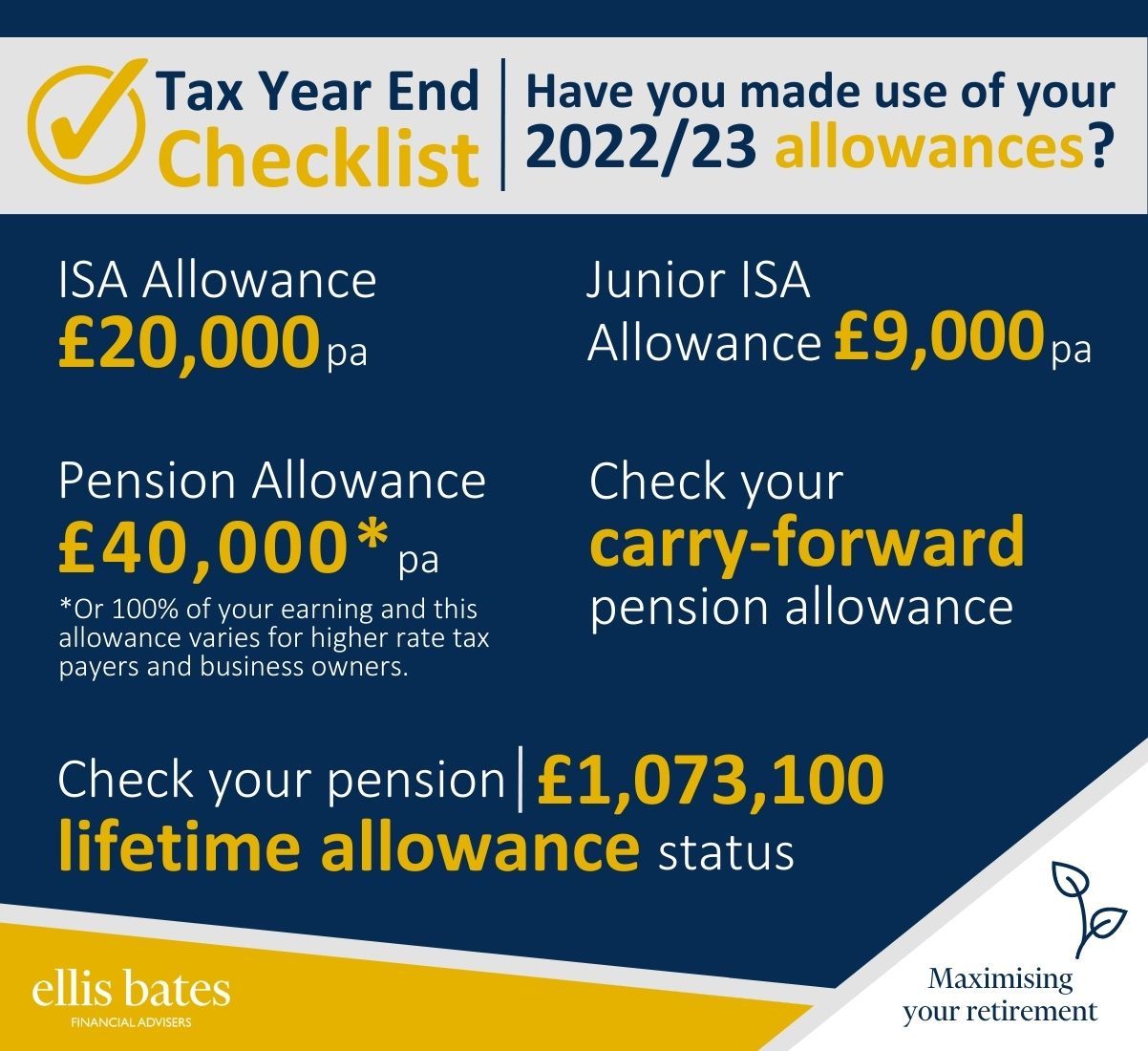

Checklist for Protecting your Family’s Finances

https://www.ellisbates.com/wp-content/uploads/2023/02/Checklist-for-Protecting-Your-Familys-Finances-infographic-holder.jpg 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

Checklist for Protecting your Family’s Finances

Create an estate plan

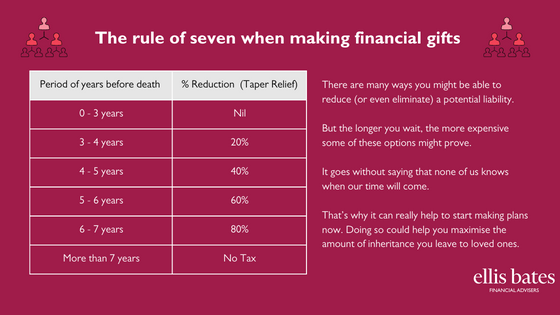

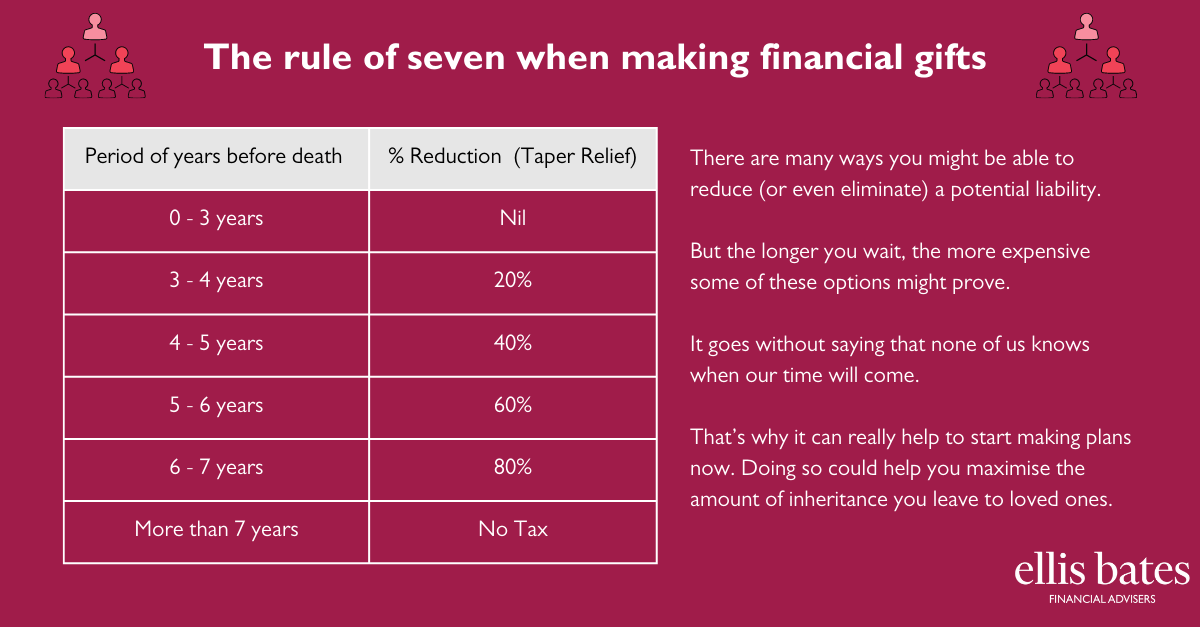

Estate planning isn’t only for the wealthy. There are various ways you can minimise Inheritance Tax like gifting or utilising pensions and trusts.

Protect against illness and death

We can help select the right products for you and your family’s needs.

Write or review your Will

Ensure your money and assets go to the people and causes you care about.

Get in touch

For more information on our inheritance tax planning services, please get in touch.