Retirement vs Cost of Living Crisis

https://www.ellisbates.com/wp-content/uploads/2022/12/Funding-the-retirement-lifestyle-you-want-vs-the-cost-of-living-560-×-315px.png 560 315 Jess Easby Jess Easby https://secure.gravatar.com/avatar/70f816837c455030814d46a740cfc12d89893aaf8cbf8c8f8f59387d7b30ac08?s=96&d=mm&r=g

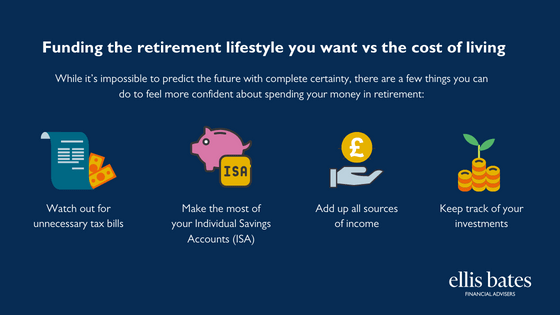

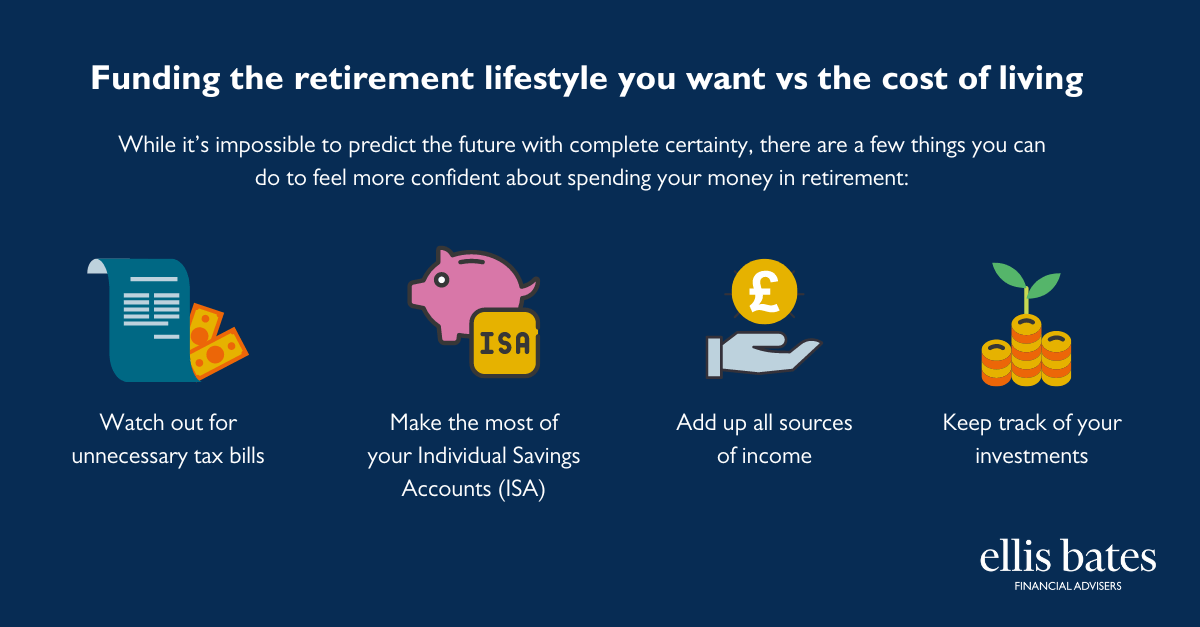

Funding the retirement lifestyle you want vs the cost of living

While it’s impossible to predict the future with complete certainty, there are a few things you can do to feel more confident about spending your money in retirement:

- Watch out for unnecessary tax bills

- Make the most of your individual savings accounts (ISA)

- Add up all sources of income

- Keep track of your investments