Make a Will

One of the most important components of an estate plan is a Will. First and foremost, a Will puts you in control. You choose who will benefit from your estate and what they are entitled to. You also decide who will administer your affairs after your death.

Read about our Will writing service.

Make a Lasting Power of Attorney

A Lasting Power of Attorney (LPA) can be made for Property and Financial Affairs, as well as Health and Welfare. These documents can be put in place at any time, and it is important to consider setting them up, no matter what age you are. Once you have your Will and LPA in place, the next step is inheritance tax planning.

Read about our Lasting Power of Attorney service.

Gifting while you are alive

Almost half of all Baby Boomers say they have enough personal wealth that they can afford to gift some of it away during their lifetime and this is a most tax efficient transfer of wealth.

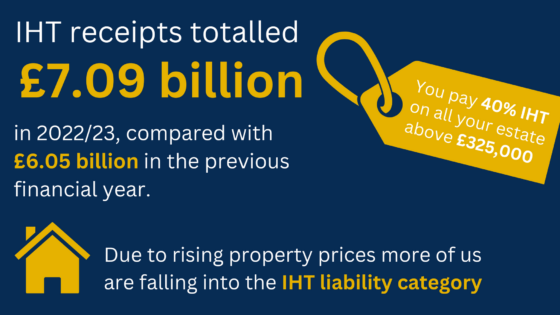

The amount is set by the government and is currently £325,000, which is frozen until 2026. In addition, since 6 April 2017, if you leave your home to direct lineal descendants, the value of your estate before tax is paid will increase with the addition of the Residence Nil-Rate Band (RNRB). For the 2021/22 tax year, the Residence Nil-Rate Band is £175,000.

One thing that’s important to remember when developing an estate plan is that the process isn’t just about passing on your assets when you die. It’s also about analysing your finances now and potentially making the most of your assets while you are still alive. By gifting assets to younger generations while you’re still around, you could enjoy seeing the assets put to good use, while simultaneously reducing your IHT bill.

Life insurance within a Trust

Writing life insurance in an appropriate Trust is one of the best ways to protect your family’s future in the event of your death. Your life insurance policy is a significant asset – and by putting life insurance in Trust, you can manage the way your beneficiaries receive their inheritance. The proceeds from the policy can be paid directly to your beneficiaries rather than to your legal estate and will therefore not be taken into account when Inheritance Tax in the UK is calculated.

Keep wealth within a pension

A defined contribution pension is normally free of Inheritance Tax in the UK, unlike many other investments. It is not part of your taxable estate. Keeping your pension wealth within your pension fund and passing it down to future generations can be very tax-efficient estate planning. If you die before 75, your pension will be passed on tax-free. However, if you die after 75, your beneficiaries will pay tax on the proceeds at their highest income tax rate. Your pension will not be covered by your Will, so you will need to ensure that your pension provider knows who your nominated beneficiaries are.

Invest in IHT-exempt assets

For experienced suitable investors, another way to potentially minimise Inheritance Tax liabilities is to invest in Inheritance Tax exempt assets. These schemes are higher risk and are therefore not suitable for all investors, and any investment decisions should always be made with the benefit of professional financial advice. One example of this is the Enterprise Investment Scheme (EIS). The vast majority of EIS-qualifying investments attract 100% IHT relief via Business Relief (BR).

Everyone has different requirements and motivations – the right solutions for you are the ones that suit your personal circumstances. We can work with you to discover what these are. Our estate planning advice service is designed to help you maximise your wealth and minimise a potential Inheritance Tax bill.