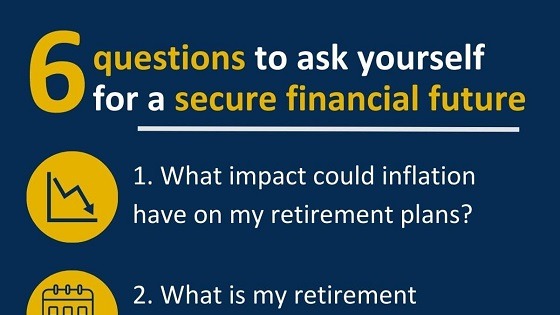

How many years do you expect to be retired?

How many years do you expect to be retired?

There are obviously no guarantees on how long any of us will live, but when it comes to retirement planning, you’ll need to make an informed guess. It’s worth considering family history, as well as factors such as your gender and geographical region. If you expect to live to around 85, but plan to retire at 55, you’ll need to save enough to support yourself for 30 years – but don’t forget, you may live a lot longer than you expect, and you’re likely to want leave something for your loved ones.

How much will your state pension be?

The State Pension rules changed radically on 6 April 2016, for men born on or after 6 April 1951 and women born on or after 6 April 1953. There is a ‘single tier’ pension payment for people in this age group with a ‘full level’. In 2022/23, the full level of the new State Pension increased by 3.1% taking it to £185.15 a week, or £9,627.80 a year.

If you reached state pension age before 6 April 2016, the changes don’t affect you. If you are married, and both you and your partner have built up a full state pension, you will receive double this amount in 2022/23 – so £283.70 a week.

How much do you have in your private pension pot?

As the State Pension is not really enough to live on, the likelihood is that workplace or private pensions will make up a significant part of your retirement income. When you retire, you have several options:

- Buy an annuity, which gives you a regular retirement income for either a set period, or for life,

- Keep your savings in your pension pot and ‘draw down’ what you need, as and when you need it.

- Keep your pot invested if you do not need the money straightaway

You will need to track down all of your pension pots and ask for a pension forecast. Estimate how much you can achieve via a drawdown, an annuity or a combination of both. Remember, the value of any investments can fall as well as rise and isn’t guaranteed.

How can you ensure your pension pot will last?

Having an understanding of your retirement income and outgoings can help you to plan for the future. Perhaps you’ve reviewed your finances and realised you can retire early, or you might decide to wait a few more years to help you boost your pension pot that bit more.

The key thing to understand is that your retirement is completely personal, and the amount you will need will depend on your specific circumstances and expectations. If you’re in any doubt about the financial impact of early retirement, you should obtain professional financial advice.

Retiring early can give you that change of lifestyle you’ve been craving, open doors to new experiences and potentially improve your health. But there are financial consequences to stopping work in your 50s.

Retiring early can give you that change of lifestyle you’ve been craving, open doors to new experiences and potentially improve your health. But there are financial consequences to stopping work in your 50s.